Chilean Mining and the New Constitution

In general, the separation between Large, Medium and Small-scale Mining is correct, particularly the last one which, through ENAMI and its purchasing power distributed throughout the country, has allowed hundreds (almost thousands) of small-scale miners or “pirquineros” (prospectors) to live an orderly and profitable life. For this segment, it is missing the application of Selective Concentration strategies for dry pre-concentrating minerals at the reception, paying only for the pre-concentrate and establishing that the pirquineros take the excess of gangue back to the places of origin, avoiding environmental pressure on ENAMI’s beneficiation facilities.

Also, it seems correct to maintain CODELCO as a company owned by the Chilean State. A few restrictions though, are related to the excessive power of unions and certain officials indicated by politicians. With some exceptions, they believe that the company belongs only to them and not to all Chileans.

Taking into consideration the environment, it should be a practice of mining companies, mainly in the northern region, to organize operations with less environmental pollution on the coast (where socio-environmental demands are more relevant) and to transfer the operations with greater impact to locations where there is less socio-environmental damage.

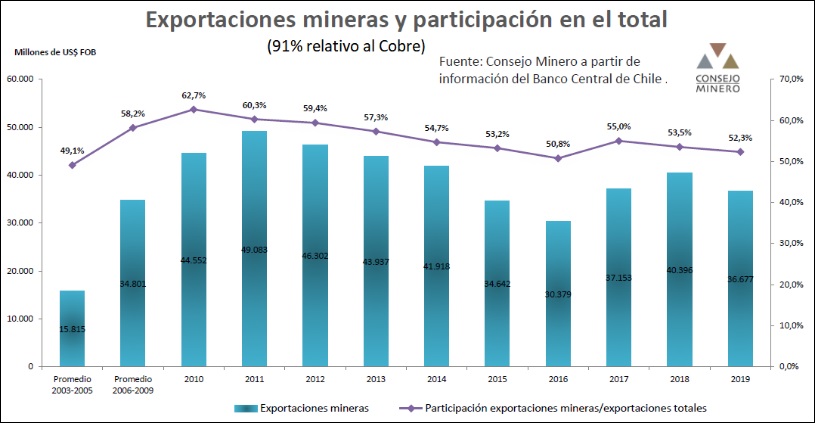

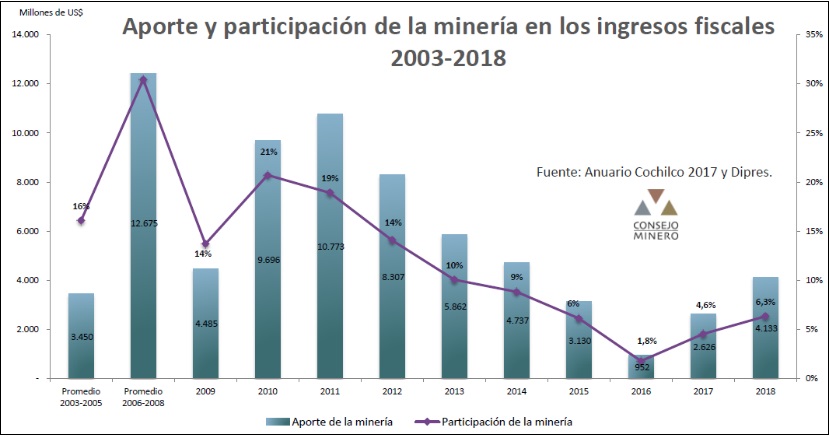

However, I consider that the biggest problem of the large Chilean mining industry (where Codelco is included) has been the gradual transfer of capital and profits to, among others, the financial sector and large suppliers of equipment and supplies, thus reducing the contribution of the mining companies to the country. Large-scale mining maintains the value of its exports and, in compensation, is reducing its contributions to the Chilean treasury. Where is the profit?

Chilean mining has been absent during these last decades, not facing technically the real problems that affect it, which are, on the one hand, the submission without proper answer to the drastic decline of the ore grades (subject that can be technically faced) and, associated to this, to the gradual transference of its profits to the financial capital and supplier companies, reducing its taxation.

The problem is not in the decrease of ore grades itself, which is a natural effect of the mining activity, but in the lack of technical confrontation to this decrease. Thus, any rock that arrives from the mine is allowed to advance until the end of the process. Nowadays it is necessary to process a ton of rock to extract only 6 kg of copper; in 2005 that same ton generate 10 kg of copper and, forty years ago, almost 15 kg of copper were produced from one ton of rock.

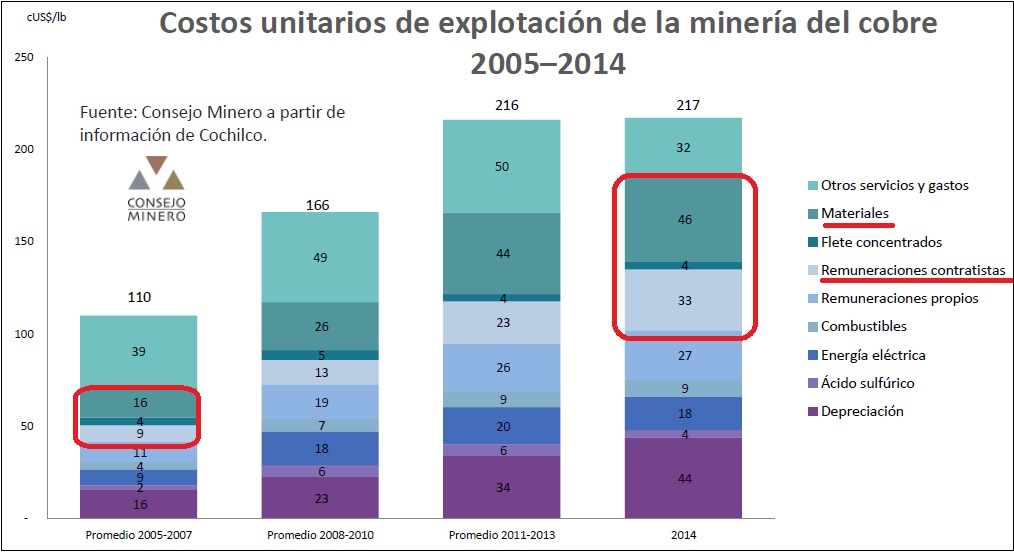

That’s the point, because of the drop in ore grades, more and more ore need to be processed to produce the same. In other words, if the Chilean mining industry maintains in all these years its same rhythm of metallic copper production (circa 5.5 MTPA), it has had to expand or implement more concentrators to treat that excess of gangue, using more capital and, still, severely increasing its costs in materials and production inputs.

The large mining companies are gradually getting into debt and transferring their capital and profits to other actors who are winning justly with the fall of the grades: the financial sector (which finds a real place to put virtual money), the global equipment manufacturing companies and global suppliers of high consumption inputs, as illustrated by the disproportionate growth in the consumption of materials and the remuneration of contractors, characterizing the management policy of the mining companies.

The constituents will now be able to correct some of these distortions, stimulating the development of strategies for technical confrontation to the fall of the ore grades, with new processing routes and bringing back the profits for the mining companies, especially CODELCO, since the “Chilean salary” is ending due to the gradual transfer of patrimony and operational cost to the financial sector, to the large global manufacturers, and to the suppliers.

Alexis Yovanovic